The five-step valuation workflow is a repeatable process for turning a large universe of stocks into a single investment decision. Stage one, Screen, uses hard filters to cut the universe to a manageable list. Stage two, Score, ranks the survivors on quality. Stage three, Value, estimates intrinsic worth as a range for the shortlist. Stage four, Document, records the assumptions and the range so the decision is auditable. Stage five, Decide, acts only when the market price clears a margin of safety below that value.

What the five-step valuation workflow is

Valuation as a craft has a well-documented middle and a neglected front and back. The middle is the model: a discounted cash flow, a set of multiples, a Graham-style formula. The front is candidate selection, and the back is the decision itself. The five-step valuation workflow names all three so none of them gets skipped. Screen and Score sit at the front and decide what deserves a model at all. Value is the middle. Document and Decide sit at the back and turn an estimate into an action you can defend a year later.

The reason to name the stages is that most errors happen in the hand-offs, not inside any single stage. An analyst runs a flawless model on a company that never should have passed a screen. A careful valuation goes unrecorded, so six months later nobody remembers which growth rate produced it. A defensible value range gets ignored because the analyst fell in love with the story and skipped the margin of safety. Naming the stages makes each hand-off visible, and a visible hand-off is one you can check.

Figure 1. The five-step valuation workflow

Each stage produces one clean output and hands it to the next: a list, a ranking, a value range, a record, and a decision.

The pillar DCF guide treats the modeling loop inside a single valuation, from normalizing data to applying a margin of safety. This workflow is the layer above it: the procedure that decides what to model in the first place and what to do with the result. The five stages below each carry one job, one output, and one hand-off.

Stage one: Screen the universe

Screening is the gate that makes everything after it feasible. The investable universe runs to thousands of names, and no investor can study them all. The first job is to remove the ones that fail a hard, mechanical test before any judgment is spent. A screen encodes disqualifiers rather than preferences. Minimum daily liquidity so you can actually trade the name. A floor on free cash flow so you screen out businesses that burn cash, or a ceiling on leverage so you skip ones that cannot comfortably service their debt. A market-capitalization band that matches your mandate. Each rule is objective, so the screen runs the same way every time and does not bend to a story.

The discipline here is to keep the screen strict and dumb. A screen is a filter, not a ranking, and its output is a list, not an order. Adding soft, judgment-heavy criteria at this stage defeats the purpose, because it drags slow human attention into a step that should be fast and automatic. Save the judgment for later gates.

Screening styles map naturally to the criteria you choose. A value screen leans on low price-to-earnings and price-to-book thresholds; a quality screen leans on returns on capital and margin stability. Apply these criteria yourself in the InvestViable stock screener, or start from a ready-made Stock Universe slice such as value stocks or quality stocks, each a coherent segment rather than the whole market. Whatever style you pick, the output of Stage one is the same shape: a defensible list, short enough that the next stage can rank it.

Stage two: Score the survivors

A screen tells you what qualifies. It does not tell you what is best. Stage two ranks the survivors so the scarce hours of Stage three go to the strongest candidates first. Scoring is triage, and like medical triage it is about ordering attention, not making the final call.

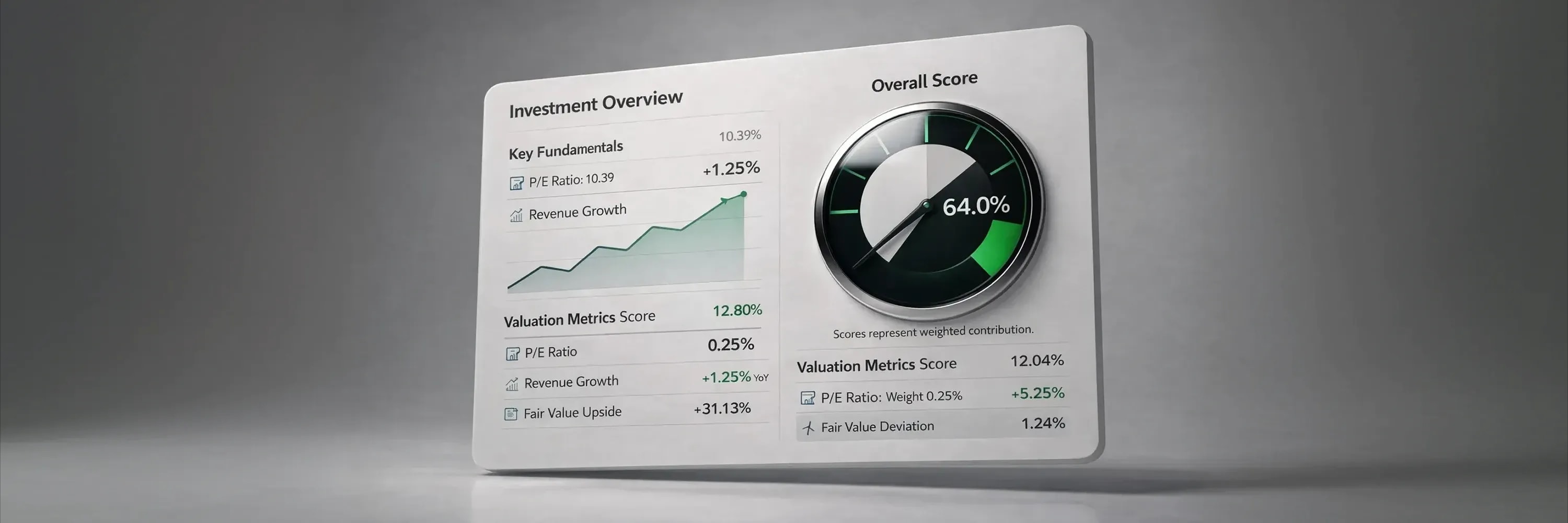

A good score is transparent about what it rewards. It aggregates checks on profitability, balance-sheet strength, capital efficiency, and consistency into a single comparable number, so a name that clears every check ranks above one that limps through on two. The InvestViable Investment Score works this way: it runs 28 checks and reports a result out of 31 points, expressed on a 0 to 100 scale. The checks sit in three categories, Valuation, Financial Strength, and Performance, with the inputs and what the score evaluates documented rather than hidden. Because it is comparable across companies, it turns a screened list into a ranked queue.

The trap at this stage is mistaking the score for the answer. A high score means a business is worth studying, not that its stock is cheap. Quality and price are separate axes: a superb company can be a poor investment at the wrong entry point, and a mediocre one can be a fair bet if it is cheap enough. Scoring resolves only the first axis. It hands the ranked queue to the Value stage, which resolves the second. Keeping those two questions apart is what stops a good score from being read as a green light.

Stage three: Value the shortlist

Now the modeling begins, and now the pillar methods earn their keep. Stage three estimates what each shortlisted business is actually worth, and the first decision is which model fits. A discounted cash flow suits companies with steady, forecastable cash flows. Relative multiples suit cyclical or erratic earners where a clean forecast is impossible. An asset or Graham-style approach suits businesses whose value sits on the balance sheet. Matching the model to the company is the substance of the intrinsic-value workflow, and getting the match wrong is a more common error than getting the arithmetic wrong.

Whichever model you choose, the output should be a range, not a single number. False precision is the classic valuation mistake. Building a bear, base, and bull case forces the uncertainty into the open and gives the Decide stage something honest to work with. The inputs deserve current sources rather than habits. Aswath Damodaran's data on equity risk premiums and costs of capital, refreshed for the year, is the practitioner reference for the discount rate. The risk-free floor tracks the current 10-year Treasury yield.

A tool keeps the arithmetic consistent across the shortlist. The InvestViable Valuator exposes three inputs in its discounted cash flow mode: the cash flow growth path, the discount rate, and the terminal growth rate. Entering the same three assumptions for every candidate, and sliding each across a plausible band, produces the value range this stage is meant to deliver and makes two companies genuinely comparable.

Stage four: Document the decision

The stage investors skip most is the one that pays off most over time. Documentation turns a valuation from a fleeting calculation into a record you can audit. It answers three questions in writing: where the numbers came from, what you assumed, and what could break the thesis. Without that record, a valuation is unrepeatable, and an unrepeatable valuation cannot be compared, revisited, or learned from.

A usable record names its sources. Pointing each figure back to a primary filing on SEC EDGAR means a future reader, including your future self, can check whether a number was current or stale. It states the load-bearing assumptions explicitly, especially the growth rate and the discount rate, because those are where reasonable people disagree and where a thesis quietly drifts. And it lists the caveats the model cannot capture, such as a regulatory overhang or a customer concentration, so the risks are on the page rather than in your memory.

Consistency is the deeper payoff. If you value one company from a detailed record and another from a scribble, you cannot compare them, and comparison is the whole point of building a shortlist. A standard record format enforces the same rigor on every name. InvestViable generates a valuation report from the Valuator's ticker page, so this documentation becomes a by-product of the work rather than a separate chore. However you produce it, the output of Stage four is a written, sourced, auditable case, ready for the only stage that touches money.

Stage five: Decide on the margin of safety

Every prior stage produced information. This one produces an action, and it hangs on a single comparison: price against value, not value alone. A business can be excellent and its stock still too expensive to buy. The Decide gate exists so that quality never gets confused with opportunity.

The rule is mechanical. Take the value range from Stage three, anchor on the base case, and set a threshold below it by your margin of safety.

Buy-below price = Estimated value × (1 − Margin of safety)

The margin of safety is not a bargain-hunting tactic; it is insurance against your own errors and the future's refusal to cooperate. Its size should scale with how uncertain the valuation is: a wider range from Stage three demands a deeper discount here. Only when the market price falls below the buy-below threshold does the workflow authorize a purchase.

Figure 2. The Decide gate: price against value and the margin of safety

Action depends on where the market price sits relative to the estimated value, less the margin of safety.

Three outcomes fall out of the comparison. If price sits below the threshold, the discount is there and you act. If price sits between the threshold and the value, the company is fairly priced but offers no cushion, so it goes on a watch list rather than into the portfolio. If price sits above the value range, you pass, however much you admire the business. The hardest of the three is the watch list, because it means holding a good idea without acting on it. That patience is exactly what the earlier stages were built to make possible.

How to run the workflow without rebuilding it each time

The five stages are a loop, not a one-way street. Screen on a schedule so the universe stays current. Score and value only when a screen surfaces something new or a holding's price moves enough to change the math. Lean on the documentation from prior passes so a familiar company starts from your own assumptions instead of a blank page. Most investors spend too long in the Value stage and too little in Screen and Document, which is precisely backwards: the upstream gate protects your time and the downstream record compounds it. The workflow also gives your research a shared vocabulary. When every idea moves through the same five stages, you can compare a name you studied today against one you studied last quarter. Both were screened, scored, valued, documented, and decided on the same terms. That comparability is what a collection of one-off valuations can never offer. If you want to sharpen one stage first, build a defensible discount rate for the Value step and enter it in the InvestViable Valuator. Then read the output as a band and let the Decide gate do its job.

InvestViable does not publish buy or sell recommendations on individual securities. All analysis is based on public financial data and a transparent methodology. The Investment Score formula is proprietary; the inputs and what the score evaluates are documented.