Introduction

Price acts as the most visible metric in financial markets. It flashes on screens, scrolls across tickers, and dominates news headlines every minute of the trading day. Value, however, remains invisible. You must dig into financial statements, assess competitive advantages, and estimate future cash flows to find it. Most beginners confuse these two concepts, but successful investing depends on your ability to separate what you pay from what you get.

This distinction is critical because the economic environment has changed. The era when you could blindly buy any asset and expect it to rise is over. BlackRock states that the period when nearly every chip you placed in the market seemed to pay off is behind us, and gambling in today's markets offers much worse odds than it did just a few years ago. This shift marks the return of an "Investor's Market," where rigorous analysis is the only reliable way to protect your capital. If you don't learn to calculate value yourself, you leave your financial future to the whims of market sentiment.

This guide walks you through a logical workflow to determine stock value based on business fundamentals rather than hype.

Disclaimer: Please note that this guide is for educational purposes only and does not constitute investment advice. This article explains valuation concepts and workflows to help you make your own decisions.

Distinguishing Price from Stock Value in an "Investor's Market"

Understanding business fundamentals begins with a clear distinction between cost and worth. The stock market frequently confuses a stock's price with the underlying business's value. Price represents the money you pay to buy a share, and this number fluctuates based on temporary sentiment, news cycles, and liquidity. Value, however, represents the present worth of the cash the company will generate for you in the future. You must view these two concepts as distinct entities that often move in opposite directions to build a rational portfolio.

Shifting economic conditions require you to approach the market differently than you might have during the recent boom years. The era of easy money has ended, which means betting on rising prices without analyzing the business is now a dangerous strategy. BlackRock's Chief Investment Officer Rick Rieder explains that market participants face changed odds. He notes that investing still offers good odds if you own durable income and strong balance sheets while giving those positions time to compound. In contrast, gambling on price action now offers much worse odds than before.

If you ignore stock value and focus only on price momentum, you risk entering a position that can't generate a return for decades. History provides stark warnings about this danger. Cisco Systems dominated the tech sector during the dot-com boom, yet its stock price detached from its business reality. The stock peaked at $80.06 in March 2000 with a P/E ratio exceeding 200, and it took 25 years and 8 months to recover to that price level even though the company quadrupled its profits during that period. This massive disconnect between price and value destroyed shareholder wealth for a generation. To avoid this trap, you must prioritize fundamental stock valuation over market hype and commit to your ongoing financial education about these principles.

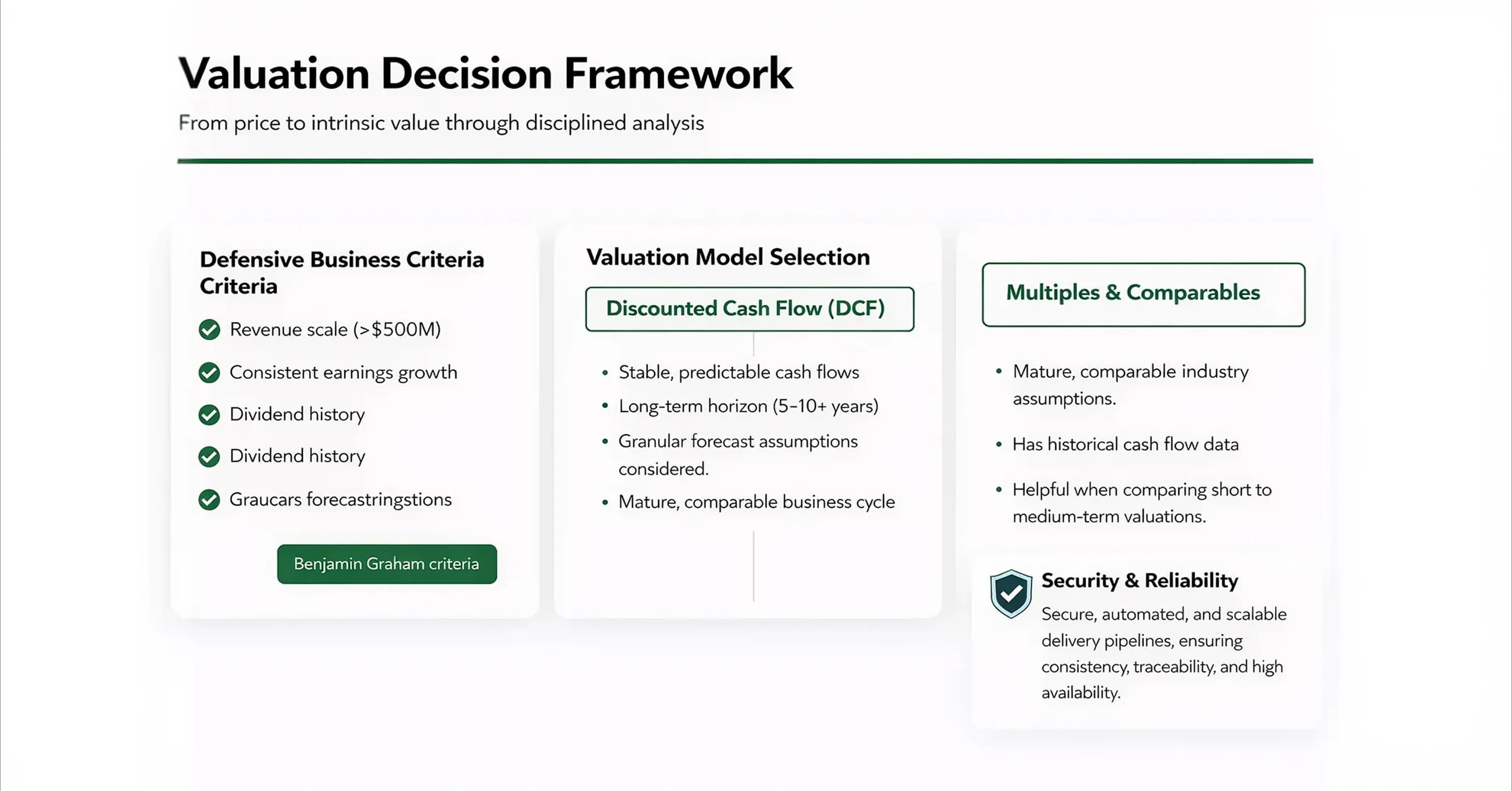

The Valuation Decision Framework

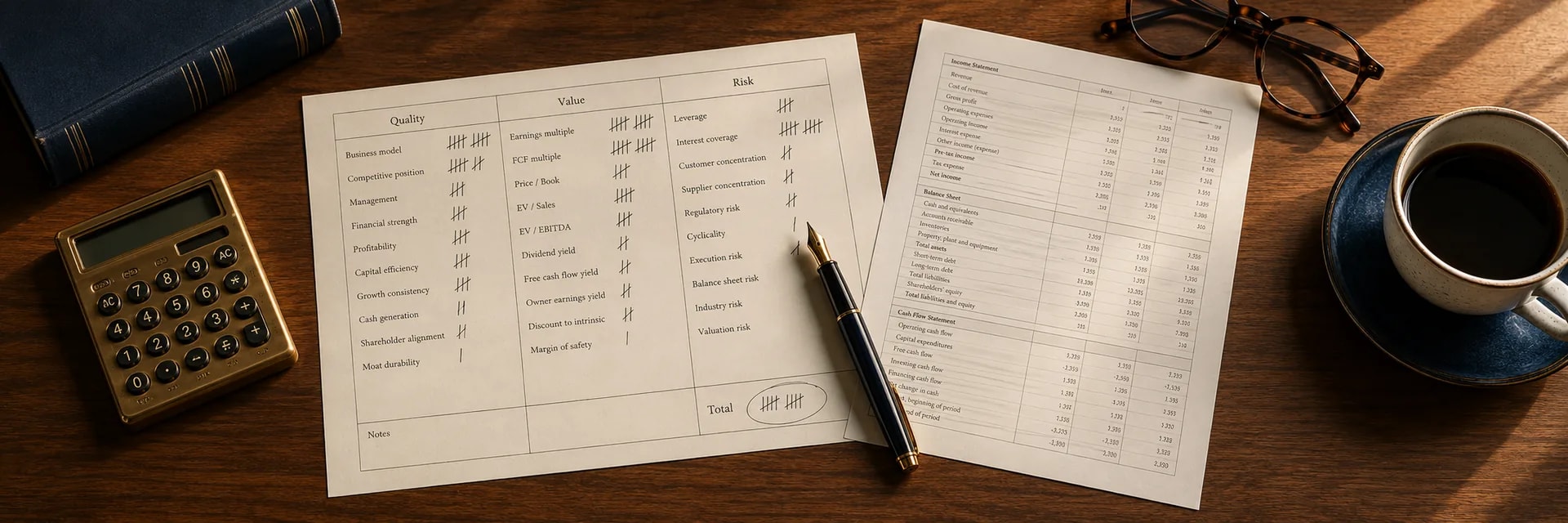

Armed with a clear understanding of price versus value, you need a system to measure it. Before you open a spreadsheet to calculate numbers, you need a decision framework to guide your analysis. A proper valuation requires matching the correct model to the specific type of company you analyze. Many investors fail because they apply complex mathematical formulas to companies that don't have predictable futures. Value investing father Benjamin Graham established strict criteria for what constitutes a defensive investment suitable for valuation. He recommended that defensive stocks have at least $500 million in annual sales, a record of positive earnings growth, and a history of paying dividends.

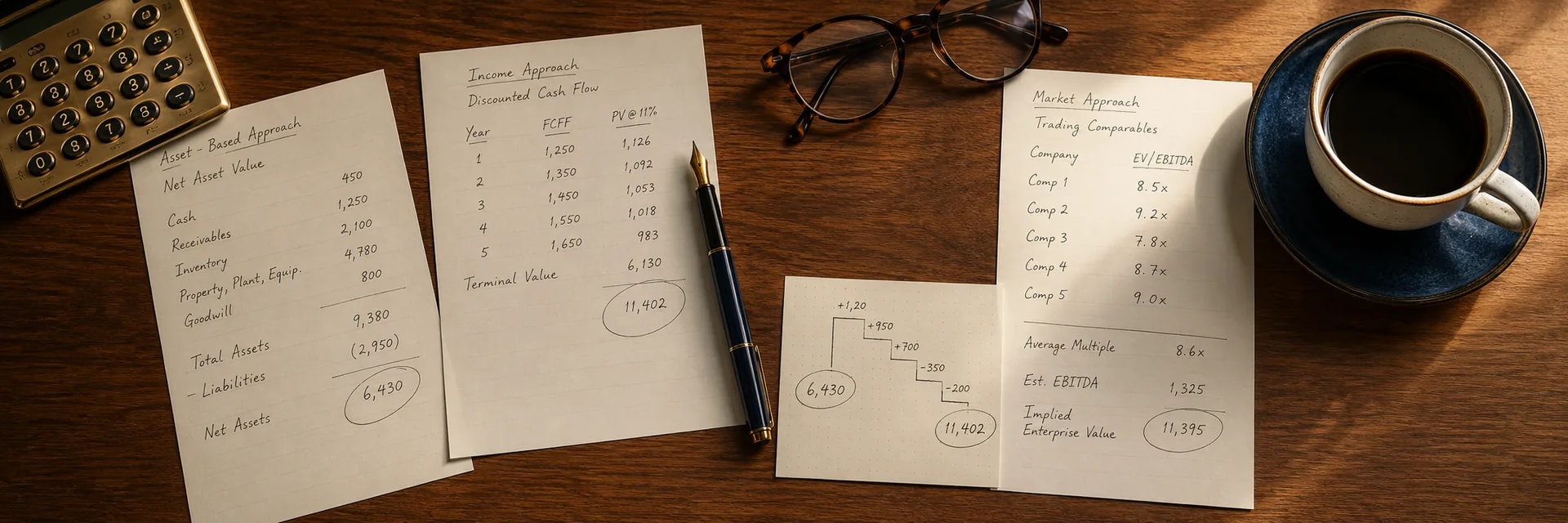

Once you confirm that a business has a stable structure, you can choose the right valuation method. A Discounted Cash Flow (DCF) model works best for companies with steady, predictable cash flows like utility companies or mature consumer goods manufacturers. This model projects future cash into the present. However, a Relative Valuation approach using multiples like P/E or EV/EBITDA compared to historical averages provides a safer estimate for companies with erratic earnings or those in cyclical industries.

This choice of fundamental stock valuation model matters because it dictates the inputs you will use. But regardless of the model, the core philosophy remains the same. Late Berkshire Hathaway vice chairman Charlie Munger advised that all intelligent investing is value investing, which simply means acquiring more than you pay for. Your goal is to determine that "more" before you spend a dime. If you strictly follow this methodology, you reduce the role of luck in your returns. By selecting the right valuations approach for each asset, you ensure that your investment decisions rely on logic rather than hope.

Inputs, Assumptions, and the Margin of Safety

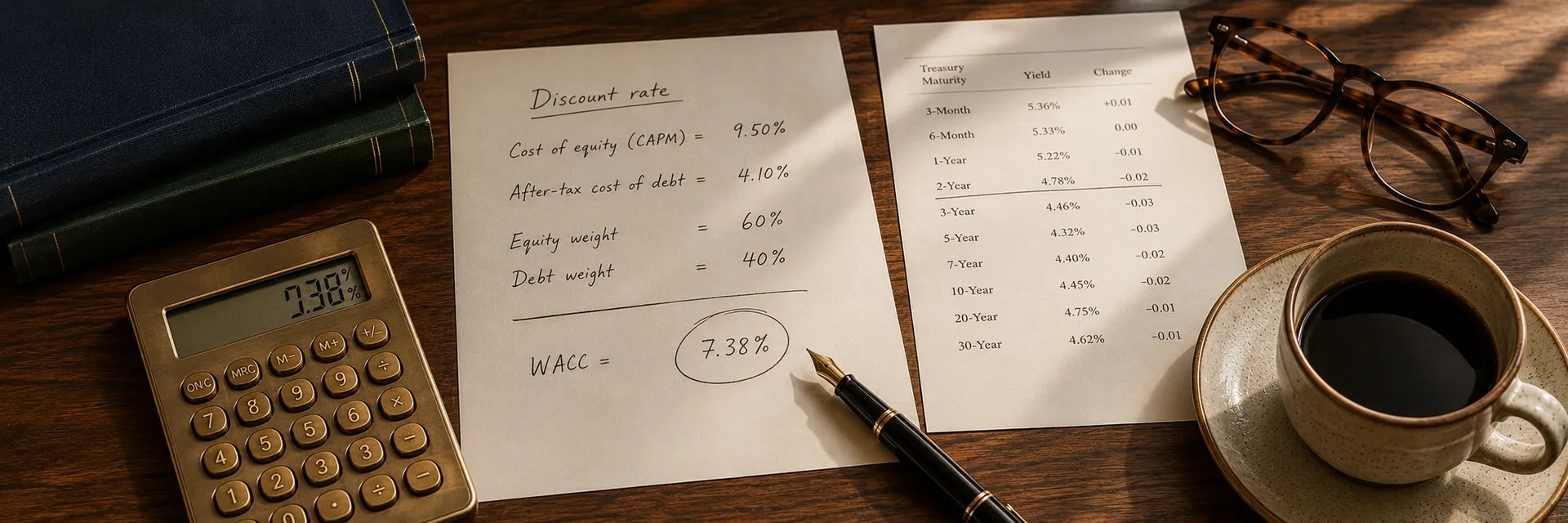

Logic requires accurate data, so you must gather the right information. To calculate stock value, you need specific financial data. You must gather figures about free cash flow, profit margins, and revenue growth. However, remain cautious with these inputs. If you enter high growth rates, your stock value calculator outputs a number that looks attractive but doesn't reflect reality. Conservative inputs protect you from disappointment.

Even if your inputs seem accurate, the future remains unpredictable. This uncertainty requires you to apply a Margin of Safety to your final calculation. This concept acts as a defensive measure against your own analytical errors and unforeseen market events. You don't apply this discount to find a bargain; you apply it to prevent capital loss.

Experienced investors treat this margin as a mandatory requirement rather than an optional bonus. Benjamin Graham and David Dodd recommended a margin of safety of 30-50% for investments, which represents the difference between intrinsic value and market value. This buffer absorbs the impact if the company performs worse than you expected. Seth Klarman emphasizes that the difference between price and fair value is your margin of safety. The wider the difference, the more protected you are from surprises. If the market price doesn't offer this safety margin after you run the numbers, you must have the discipline to walk away.

Responsible Tool Usage and Avoiding Pitfalls

Once you understand the math, you can use technology to streamline the process. Investors often rely on digital tools to speed up the analysis process. A stock value calculator can save you time, but you must treat it as an assistant rather than an authority. Automated models simply process the data you provide. If you enter incorrect data, the model will produce a flawed result. You need to perform a Discounted Cash Flow (DCF) calculation manually or audit the automated output to understand the mechanics behind the number.

You must verify specific data points that often confuse automated feeds. For instance, data providers sometimes report financial results in a different currency than the stock price, which skews the valuation significantly. Additionally, you must confirm the current share count. Many automated tools use outdated "Trailing Twelve Month" (TTM) data that misses recent share buybacks or issuances.

Stock-based compensation poses a specific danger to your accuracy because it increases the share count over time. This acts as a hidden cost that reduces your ownership stake. Research shows that the median technology company dilutes shareholders by 2.6% annually through stock-based compensation. You can't ignore this factor. In fact, zero companies with over 3% average net dilution had share prices that beat the Nasdaq index. Always perform a final sanity check on the output to ensure the valuation makes logical sense before you risk your capital.

Conclusion

Valuation is an estimate rather than a precise figure. No matter how advanced your model is, it can't predict the future with 100% accuracy. The workflow's goal isn't to give you a magic number, but to protect you from overpaying for a business. You build a defense against market volatility and human error by distinguishing price from value and applying a margin of safety.

The market will likely continue to oscillate between extreme optimism and pessimism. Your job is to remain rational when others are emotional. Pick one stock you currently own or plan to buy and apply this "Price vs. Value" check. Run the workflow, verify the inputs, and see if the current market price offers you a sufficient margin of safety. If you treat stock value as your primary guide, you will stop gambling and start investing.