Choosing which valuation method to use depends on the company, not on taste. Use discounted cash flow (DCF) when free cash flow is predictable; use relative valuation with multiples when you need speed, sector context, or a check on a company with erratic earnings; use the Graham formula for stable, profitable, moderate-growth businesses. When a company is unprofitable, deeply cyclical, or asset-heavy, lean on normalized earnings, a reverse DCF, or an asset-based view. Disciplined analysts run more than one method, treat each result as a range, and study why the methods disagree rather than averaging them.

Why method selection comes first

Deciding which valuation method to use is the first analytical move, and it carries more weight than the precision of any single calculation. The methods are not interchangeable lenses that should agree if you are careful enough. Each one encodes an assumption about how a company creates value, and applying it to a business that violates that assumption all but ensures a poor estimate no matter how clean the inputs are.

A discounted cash flow model assumes you can forecast cash flows with enough confidence to discount them. A multiple assumes a peer group prices the same economics you are buying. The Graham formula assumes steady earnings and a normal growth rate. Match the assumption to the company and the math becomes a useful estimate. Violate it and the math becomes a way of dressing up a guess.

This is why the same stock can look cheap on one method and expensive on another, and why that disagreement is where the analysis becomes most useful. Aswath Damodaran frames valuation as a craft of matching the approach to the asset rather than defending one universal model. The selection decision is also where confirmation bias does the most quiet damage: an investor who has already decided to own a company will gravitate to whichever method flatters it. Choosing the method on the company's characteristics, before you look at the answer, is the discipline that keeps the rest of the work honest.

The questions that pick the method by company type

You do not choose a valuation method by topic or sector label. You choose it by answering a short sequence of questions about the company's economics, and the right tool falls out of the answers. The decision turns on five characteristics: how predictable the cash flows are, whether earnings are positive and stable, whether the company returns cash through dividends, how capital-intensive the business is, and how cyclical its results are.

Figure 1. A decision path for choosing a valuation method by company type

Answer the questions in order; the first branch a company fails routes it to the method built for that situation.

Predictable cash flow is the single most important fork. A mature consumer-staples company with decades of stable demand answers yes and points toward an absolute, cash-flow-based method. A semiconductor maker whose earnings triple and halve with the cycle answers no, and forcing a smooth forecast onto it manufactures false confidence. Profitability is the next fork: a company with no earnings cannot be valued on earnings-based shortcuts at all. Dividend policy, capital intensity, and cyclicality then refine the choice among the remaining methods. A capital-light software firm with recurring revenue and a capital-heavy pipeline operator can both be profitable, yet they reward different lenses, because the durability and visibility of their cash differ. Working the questions in order, rather than reaching for a familiar model, is what separates a defensible valuation from a rationalized one. The point is to let the company's economics nominate the method before any number is entered.

When discounted cash flow (DCF) fits

Discounted cash flow (DCF) is the natural method when a business produces free cash flow you can forecast with reasonable confidence. It values a company directly on the cash it generates for owners, discounted to today, which makes it the most direct intrinsic approach and the one least dependent on the market's current mood. Mature businesses with durable demand, stable margins, and a clear reinvestment pattern are where DCF earns its reputation: regulated utilities, established consumer brands, and entrenched industrial suppliers all fit the profile.

The strength of DCF is also its hazard. Because the output depends on a multi-year forecast, small changes in the growth rate or discount rate move the answer substantially, so the method rewards conservative, well-sourced inputs and punishes optimistic ones. Anchor the discount rate to observable data; the 10-year Treasury yield is the standard risk-free starting point, with the equity risk premium and any company-specific risk layered on top. Before trusting any output, work through the full DCF methodology and stress-test the assumptions rather than the conclusion.

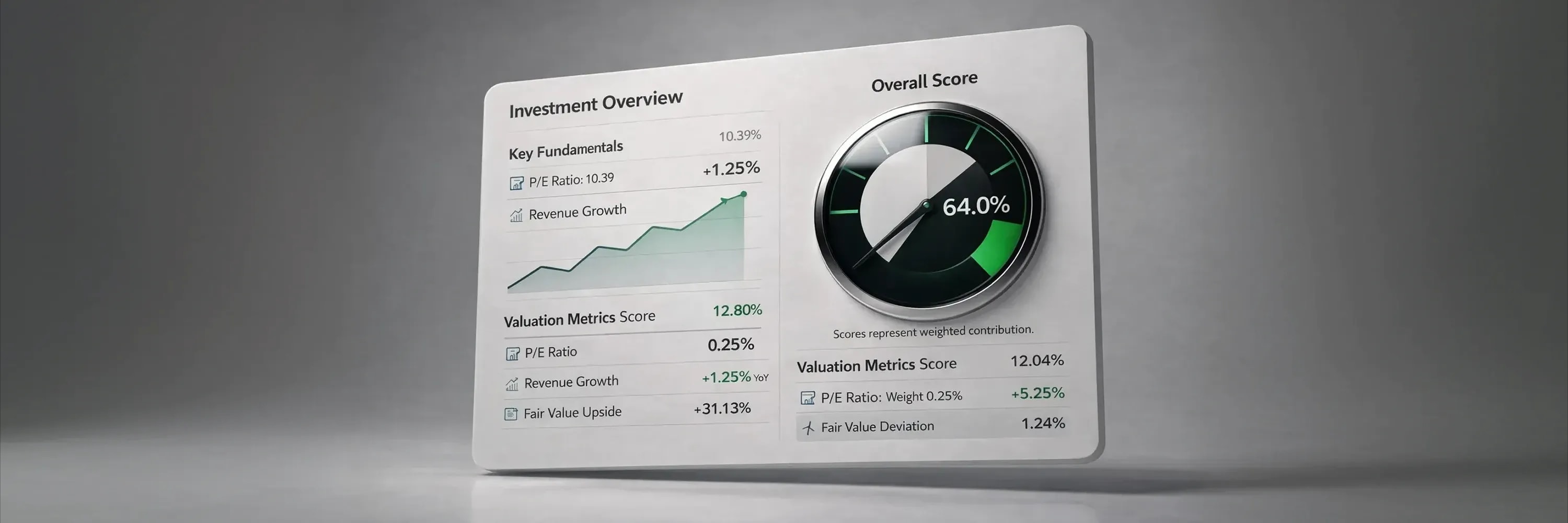

The InvestViable Valuator runs the DCF from three explicit inputs: the cash-flow growth path, the discount rate (shown as the expected return you require), and the terminal growth rate. Keeping the inputs visible is the point, because a valuation you cannot interrogate is one you cannot defend. DCF is the wrong first method, though, the moment cash flows stop being forecastable, which is exactly when investors reach for it most and should reach for it least.

When relative valuation with multiples fits

Relative valuation prices a company against its peers using ratios such as price-to-earnings or enterprise-value-to-EBITDA. It answers a different question than a DCF: not what a business is worth in absolute terms, but what the market currently pays for similar economics. That makes multiples the right tool when you need speed, when you want sector context for a DCF you have already built, or when a company's earnings are too erratic to forecast cleanly but its peer group is well defined.

The method carries a structural weakness you cannot engineer away. A multiple inherits the mood of its peer group, so if the whole sector is priced richly, a stock that looks cheap relative to peers may still be expensive in absolute terms. Choosing the right ratio for the right business is its own discipline; the guide to industry benchmark multiples covers which multiples suit which sectors and why a single number rarely travels across industries.

Low multiples also deserve skepticism rather than reflexive enthusiasm. Research on equity pricing finds that about 75% of the cross-sectional dispersion in price-to-earnings ratios reflects expected future returns rather than earnings growth. In practice, a low ratio often signals higher required returns, frequently compensation for risk the market has already priced rather than a bargain it has missed. Use multiples to triangulate and to move quickly, and pair them with an absolute method whenever the verdict actually matters.

When the Graham formula fits

The Graham formula, drawn from Benjamin Graham's work on the defensive investor, estimates a rough intrinsic value from earnings, a growth assumption, and an adjustment for prevailing high-grade bond yields. It suits exactly the kind of company Graham built it for: profitable, financially sound, and growing at a moderate, believable pace. For a stable business with a long record of positive earnings, the formula offers a fast, transparent sanity check that requires far fewer assumptions than a full DCF, which is precisely why simpler models often travel better. Damodaran argues that simpler valuation approaches are often more reliable than complex ones because added complexity tends to introduce spurious precision rather than accuracy.

The formula's limits are sharp, and respecting them is the whole skill. It assumes durable earnings, so it overstates value for a cyclical company caught at a peak and breaks entirely on an unprofitable one, returning a number that looks authoritative but means nothing. Graham guarded against this by pairing the formula with strict quality criteria rather than applying it indiscriminately.

Used as a screen, this logic scales well. The InvestViable stock screener screens the full US universe on fundamentals and the Investment Score, comparing price against fair value. A Stock Universe slice such as value stocks starts from names trading below a conservative fair value estimate. That keeps the approach pointed at the companies it was designed to evaluate rather than the value traps a price-only filter would flag as cheap. The Graham formula is a starting filter for stable compounders, not a universal valuation engine.

Where all three methods break

Some companies refuse to fit any of the three primary methods cleanly, and recognizing those cases is part of choosing well. An early-stage, unprofitable company has no steady earnings to capitalize and no forecastable cash flow to discount, so a naive DCF and the Graham formula both fail. A deeply cyclical business reports earnings that mean little at any single point in the cycle. An asset-heavy or financial firm carries value on its balance sheet that an earnings lens can miss entirely.

Figure 2. How well each method fits common company profiles

A directional fit matrix: which method to lead with for each kind of business, and where each one weakens.

For these edge cases, the workaround is to change the input rather than abandon the discipline. Normalizing earnings across a full cycle restores meaning to a cyclical company's figures before any model runs. A reverse DCF flips the problem, asking what growth the current price already assumes. For a richly priced or hard-to-forecast name, judging whether that implied growth is achievable is often more honest than building a forecast from scratch. An asset-based or book-value view, summing net assets rather than capitalizing earnings, sets a floor for financial and asset-heavy firms where the balance sheet drives worth. Whichever workaround applies, the honest result is a wider range, and that width is itself information. Building and reading those valuation ranges as a bear-base-bull spread keeps the uncertainty visible instead of hiding it behind a single false-precise number. A dedicated treatment of valuing unprofitable companies is a deeper subject in its own right.

How to apply this

Answer the selection question before you run any numbers: what kind of company is this, and which method does its economics actually support? Predictable cash generators point to DCF, erratic or peer-defined businesses point to multiples, stable profitable compounders suit the Graham formula, and the awkward cases call for normalized earnings, a reverse DCF, or an asset-based floor. Reading filings on SEC EDGAR rather than aggregated summaries is how you judge predictability honestly, because the footnotes reveal whether reported earnings recur. Whichever method you choose, apply a margin of safety to the result, scaling the discount you demand to how much the method had to assume. Where method selection sits inside the broader intrinsic value workflow is worth understanding so the choice connects to the steps before and after it.

Then run more than one method, hold each result as a range, and treat disagreement between them as the signal it is. On InvestViable, every stock page shows three base valuations side by side, a DCF, an EBITDA Multiple estimate, and Earnings Fair Value, so you can see how much the method you trust changes the answer. The method you choose shapes the answer more than any single input, so choosing it deliberately is the highest-leverage decision in the whole process.

InvestViable does not publish buy or sell recommendations on individual securities. All analysis is based on public financial data and a transparent methodology. The Investment Score formula is proprietary; the inputs and what the score evaluates are documented.