A stock valuation report exists to make a valuation reconstructable, comparable, and defensible. The intrinsic value is one line of it. The thesis, the documented assumptions, the value range, and the risks are the rest, and they give the number meaning after the day it was calculated.

What a stock valuation report is, and why the number is not the deliverable

A stock valuation report is the written record of a completed valuation. It is not the calculation that produced the number. The distinction matters, because the calculation and the document serve different purposes. The calculation answers a private question for the analyst: what is this business worth under a given set of assumptions? The report answers a durable question for the analyst's future self and for anyone who inherits the work. Why is that the number? What does it depend on? Under what conditions would it be wrong?

The number alone fails three tests that the report passes. The first is reconstruction. A bare intrinsic value carries none of the reasoning that justified it, and that reasoning decays from memory faster than the number does. The second is comparison. Two intrinsic values produced by undocumented processes are not comparable. The analyst cannot tell whether the gap between them reflects two different businesses or two differently sloppy models. The third is defensibility. A number with no written assumptions behind it cannot be challenged on a specific input. A colleague can only accept it whole or distrust it whole.

Writing the report is also a quality check on the valuation. Forcing the assumptions onto the page surfaces the ones that were never examined. Consider an analyst who has to write that the model assumes operating margin expands by four points over five years. In the act of writing it, they notice whether the assumption was reasoned or inherited from a default. The report is part of the analysis itself. Producing it tends to improve the conclusion it records.

The anatomy of a valuation report template: seven required sections

A valuation report template is a fixed structure the analyst fills in for every ticker. The structure does not change issuer by issuer; only the content does. This stability is the point. Every report shares the same seven sections in the same order. Two reports can then be placed side by side and compared section against section, instead of read end to end as unrelated documents. The template imposes the comparability that ad-hoc write-ups never achieve.

Figure 1. The seven sections of a stock valuation report

A fixed structure the analyst reuses across tickers. The content changes issuer by issuer; the section order does not, which is what keeps reports comparable across a portfolio.

The first section is the thesis: one sentence stating why the business is mispriced and what the market is getting wrong. If the analyst cannot compress the case into a single sentence, the case is not yet clear enough to value. The second section is the business snapshot: what the company does, how it earns money, and where its revenue concentrates. The third is the quality and financial-strength read. This is the structural assessment of durability and solvency that decides whether the business deserves a forward projection at all. The disqualifying checks that belong here are developed in the stock-analysis safety checklist, which the report references rather than repeats.

The fourth section is the valuation itself, with the model named and the key assumptions stated explicitly. The fifth is the intrinsic-value range across downside, base, and upside cases. The sixth is the risk section, the written list of conditions that would break the thesis. The seventh is the decision-and-monitoring note: the maximum-acceptable price the range implies after a margin-of-safety discount, and the short list of inputs to watch. These last sections are detailed below. Most retail write-ups are thinnest exactly here.

Documenting assumptions: every input needs a source, a date, and a basis

The valuation section is only defensible if every input it rests on is documented. The discipline is simple to state and hard to maintain: each input carries three tags. A source records where the figure came from. An as-of date records when it was true. A basis records what kind of figure it is, audited or estimated, reported or adjusted. An input with all three tags can be challenged precisely. An input with none is an assertion the reader has to take on trust.

Historical fundamentals trace back to the issuer's filings. The most recent annual and interim reports on SEC EDGAR supply trailing revenue, margins, depreciation, capital expenditure, and working-capital movements. The report records the filing date and the period-end date alongside each. The discount-rate inputs trace to public references. The risk-free component comes from the current 10-year Treasury yield published by FRED. The equity risk premium and the unlevered industry beta, relevered to the issuer's capital structure, come from Aswath Damodaran's published datasets at NYU Stern. The forward-looking inputs are the revenue path and the margin trajectory. These are the analyst's own judgment, and the report flags them as such, so the reader knows which figures are sourced and which are reasoned. The verification questions to run on each input are set out in the DCF inputs checklist.

The basis tag prevents the most common documentation error: mixing reported and adjusted figures inside one model without saying so. Take a margin built on management-adjusted earnings, paired with a share count on a basic rather than diluted basis. Each can look reasonable in isolation. Together they produce a value that no consistent accounting would support. Recording the basis on every input makes the inconsistency visible. A report might state "operating margin on a GAAP basis" and "diluted weighted-average share count under the treasury-stock method." Writing the basis down forces the analyst to pick one convention and hold it across the model.

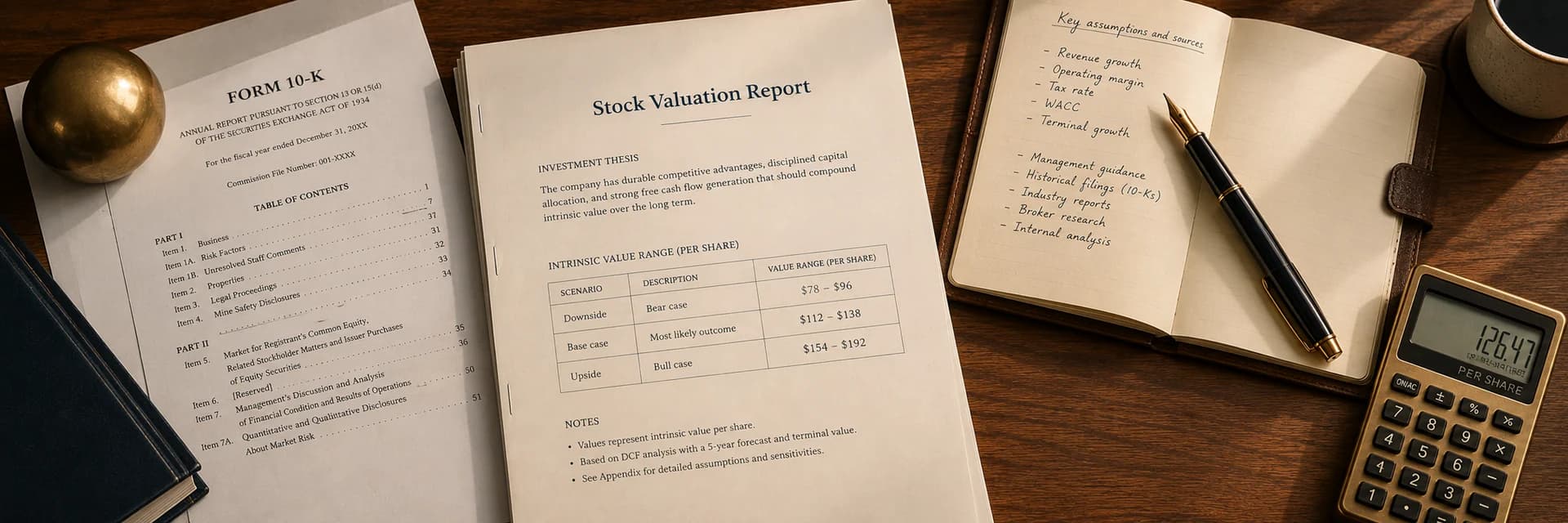

Presenting the output as a range

The valuation produces an intrinsic-value range, and the report presents it as a range. A single number invites the reader to anchor on a precision the model does not possess. The third decimal place of a discounted cash flow output is noise dressed as signal. A documented band states the uncertainty honestly. The range comes from running the same model three times: a base case on the central inputs, a downside case on conservative inputs, and an upside case on aggressive but plausible inputs. The band the three cases produce is the report's headline output.

Figure 2. Presenting the output as a value range

The report carries a downside-base-upside band, the margin-of-safety discount applied to it, and the current price plotted against the result. The relationship, not a single fair value, is what the decision reads.

Alongside the band, the report states which inputs drive it. A sensitivity note identifies the two or three assumptions that move the output most. In a cash-flow model these are almost always the discount rate and the terminal growth rate. This note does real work. It tells the reader where the conclusion is fragile and where it holds, which is what the margin-of-safety decision needs. A value that swings widely on a half-point change in the discount rate is one kind of finding. A value that holds steady across the plausible input range is another, even when both report the same base case. The discipline of building cases and reading sensitivity is developed in the CFA Institute Research Foundation's equity valuation publications.

Sometimes more than one method has been run. The report then shows the methods separately before reconciling them, instead of blending them into one figure. It presents a cash-flow range next to a multiples range, and notes where they overlap and where they diverge. That preserves the independent signal each method carries. The reconciliation discipline weights the methods by how well their assumptions fit the business. The guide to why valuation methods disagree and what to do about it develops it. The report keeps the divergence visible instead of hiding it behind an average.

The risk section: write down what would break the thesis

The risk section is the part of the report most retail write-ups skip, and the part a disciplined report treats as mandatory. Its purpose is falsification. The thesis section states why the business is mispriced; the risk section states the specific conditions under which that thesis is wrong. Writing these conditions down before committing capital is the single most effective guard against the confirmation bias that turns an analysis into an advocacy document.

The discipline is to write the risk section as a pre-mortem. The analyst assumes the thesis has failed and works backward to the cause. The causes cluster into a few categories. A key assumption proves wrong: the revenue path or the margin trajectory the value depended on. A structural quality deteriorates: a moat erodes, or leverage rises past what the balance sheet can carry. Or a piece of input data turns out to be unreliable, which is why the report records sources and bases in the first place. Each named risk is paired with the observable signal that would confirm it. The monitoring note in the final section then has something concrete to watch.

A well-written risk section also disciplines the conviction the rest of the report projects. A thesis with no credible risks usually signals a thesis that has not been examined hard enough. Forcing three or four specific, falsifiable risks onto the page calibrates the analyst's confidence against the real fragility of the case. A report that survives this section with its thesis intact carries more weight than one that never attempted it.

Reporting standards that make a report auditable and shareable

A report is auditable when a colleague can trace any conclusion back to its source without asking the author a question. It is shareable when that colleague can read it cold and understand both the case and its limits. Three standards get a report there. The first is versioning. Every report carries a date, and after the first revision a one-line note on what changed and why. The version stamp makes staleness visible, because a report whose inputs predate the issuer's latest filing is no longer current. The second is source completeness. No figure in the report appears without its source, its as-of date, and its basis, the same three tags the valuation section requires. The third is the standing non-advisory caveat. The report documents what a business is worth under stated assumptions, and it states plainly that this is analysis rather than advice to transact.

These standards are easier to hold when a tool enforces them. A stock valuation report generator applies the same structure to every report. That structure stops the analyst from quietly dropping the risk section under deadline pressure. The generator can be a self-built workbook or a platform feature. The InvestViable Valuator builds a valuation from three forward inputs: the cash-flow growth path, the discount rate, and the terminal growth rate. The separate Report Builder then turns a completed valuation into a shareable report. A self-built valuation framework template and a platform generator reach the same documented output by different routes.

The quality read the report records can also draw on a standardized score. This saves a fresh write-up on each ticker. The InvestViable Investment Score evaluates each issuer against 28 checks. The checks are scored out of a fixed denominator of 31 points and scaled to a 0 to 100 reading, across three categories: Valuation, Financial Strength, and Performance. That gives the quality-and-financial-strength section a consistent input across tickers. The report cites the score as one documented signal among several. It does not outsource the conclusion to the score. A standardized input keeps the section comparable across positions, which is the comparability goal the template serves everywhere.

Where the report fits in your workflow

The valuation report sits at the seam between analysis and decision. Everything upstream of it produces raw material. A screen narrows the universe, the safety checklist disqualifies fragile issuers, and the valuation model turns the survivors into an intrinsic-value range. The report gathers that material into one documented place. Everything downstream of it consumes the report. A margin-of-safety discount converts the documented range into a maximum-acceptable price. That discount is calibrated to the business, as set out in the margin of safety operational definition. The monitoring note then tracks whether the inputs the conclusion rested on still hold.

The payoff compounds across a portfolio. A single report is a record of one decision. A library of reports built on the same template is a comparable history of every decision the analyst has made, with the reasoning preserved next to each outcome. That history is where an investing process improves. It lets the analyst return to a thesis that worked or failed and read which assumptions carried it. The last report on paper is what makes the next valuation better.

InvestViable does not publish buy or sell recommendations on individual securities. All analysis is based on public financial data and a transparent methodology. The Investment Score formula is proprietary; the inputs and what the score evaluates are documented.