Disclaimer: This article serves educational purposes only and does not constitute investment advice. Strategy recipes function as starting configurations for idea generation, not as automatic buy decisions.

Prerequisites: data normalization

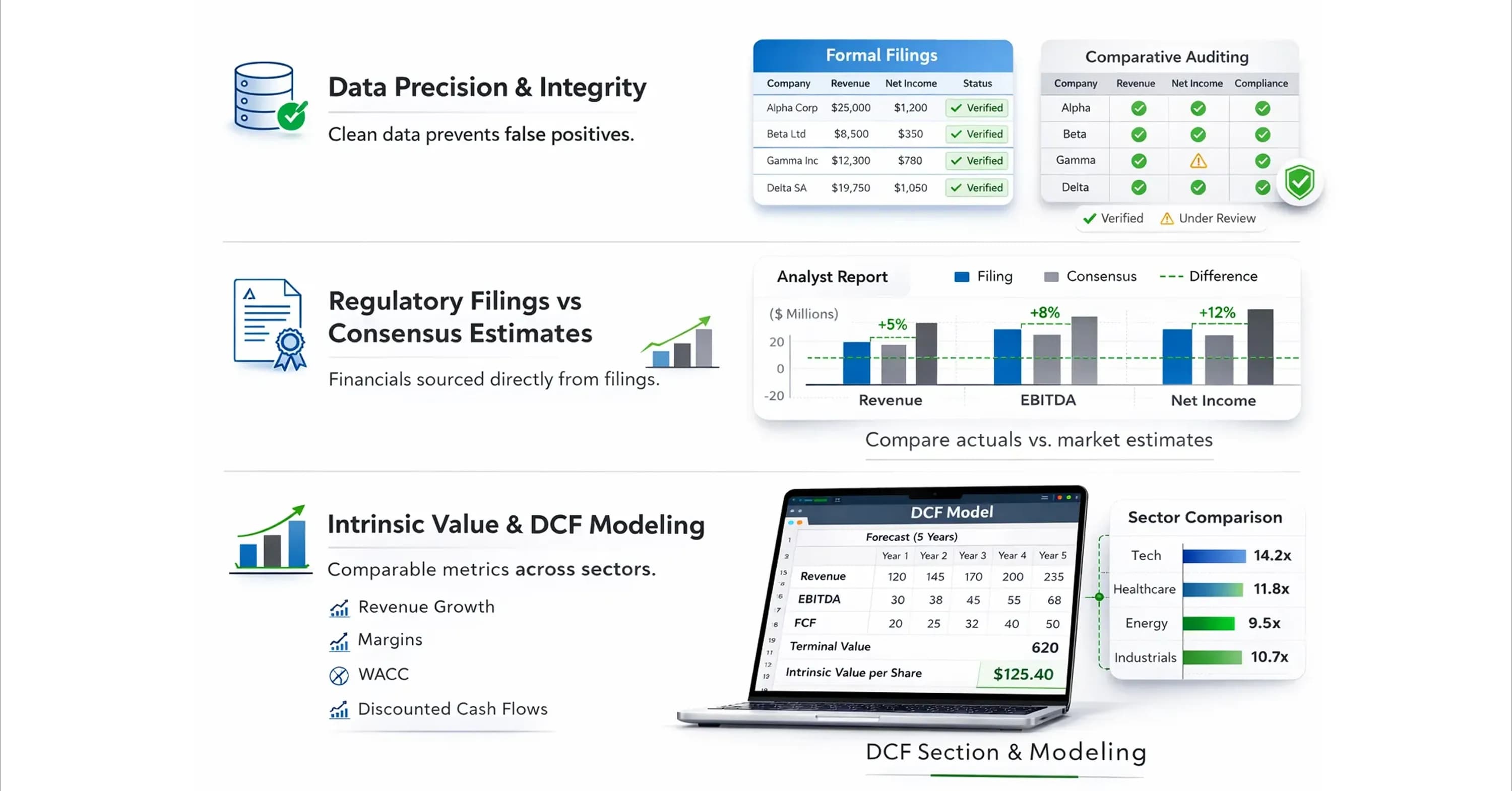

This filtration process relies on accurate inputs to function correctly. The integrity of a scan depends entirely on the quality of the data that feeds it. Investors often find that different market scanners produce different results for the same query, and this discrepancy usually stems from how platforms handle data normalization. Financial statements follow different reporting standards, such as GAAP in the US and IFRS internationally, and this creates inconsistencies in raw data. Platforms must adjust these numbers to make them comparable. For example, Morningstar systematically adjusts financial statements to ensure comparability across different companies, industries, and nations.

Without these adjustments, screening metrics can be misleading. One often-overlooked distortion comes from changes in share count over time. Share dilution occurs when a company issues new shares through mechanisms such as stock-based compensation or secondary offerings. This reduces the ownership stake of existing shareholders and can quietly inflate per-share metrics, making a business appear more profitable than it is.

Conversely, share buybacks reduce the share count and tend to reflect management's confidence in the business, as they concentrate value for remaining shareholders. Warren Buffett has long emphasized that buybacks only create value when shares are purchased below intrinsic value, so the context behind a company's capital allocation decisions serves as an important qualitative signal when reviewing scan results.

Therefore, granular universe selection serves as the first configuration step. Filters for reporting standards and liquidity thresholds exclude micro-cap stocks that lack reliable data or sufficient trading volume. This ensures that the subsequent key financial ratios used in the scan apply to businesses with verifiable financial health. The InvestViable platform applies this logic through its global screening functionality, and investors can explore these methods directly on the platform.

Foundation: filter for quality first

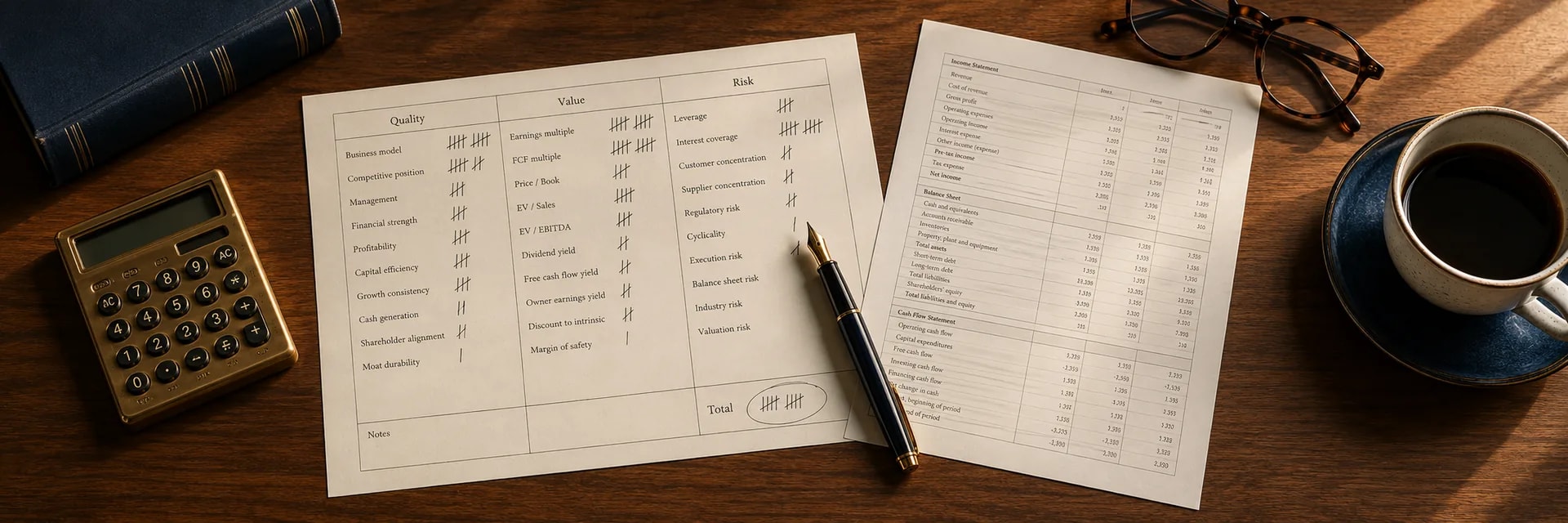

Clean data allows the investor to establish a hierarchy of metrics. A common mistake involves prioritizing valuation metrics, like a low P/E ratio, before quality. This approach often leads to value traps. Companies that appear cheap but suffer from eroding business models. Effective stock scanners place quality filters at the top of the logic tree. This ensures that every result represents a business with a durable competitive advantage before the investor even considers the price.

Historical performance data validates this sequence. AQR Capital Management demonstrated that small-cap quality stocks outperform large quality stocks, while small "junk" stocks significantly underperform large junk stocks. This reinforces the need to filter for quality aggressively, especially when scanners apply equity scan strategies to smaller companies.

Even simple methodologies follow this logic. The Magic Formula, for instance, uses Return on Capital and Earnings Yield as its two primary ranking metrics. This combination forces the scanner to identify companies that are both efficient at generating returns and trading at a fair price, rather than simply look for the cheapest assets available.

Assess Financial Health with Piotroski F-Score

Efficiency metrics require support from broader financial health indicators. Composite metrics like the Piotroski F-Score further automate the quality assessment. This scoring system aggregates nine discrete binary signals into a single number between 0 and 9, and provides a quick snapshot of a firm's financial trend. The score evaluates profitability, leverage, and operating efficiency, including metrics such as ROA, change in margins, and change in leverage.

The F-Score acts as a powerful safety filter. Historical testing from 1976 to 1996 showed that a portfolio of high F-Score stocks outperformed a low F-Score portfolio by 7.5% annually. A minimum F-Score requirement of 6 or 7 eliminates companies with deteriorating balance sheets or weakening cash flows, regardless of how attractive their valuation might appear.

Delta in Fundamentals

Current financial health scores filter out immediate risks, but they do not predict future improvement. Static metrics provide a snapshot of current health, but the market often prices this known information efficiently. Investors focus on the delta because it represents the rate of change in these fundamentals. They identify a positive growth trajectory before it becomes obvious to the broader market. Market scanners are most useful when they detect these improvements, and they compare current quarterly performance against longer-term trailing averages.

The relationship between revenue growth and operating margin expansion represents a critical divergence. Companies often suffer from inefficiency or pricing pressure when they grow revenue while margins contract. For example, Ford's operating margin decreased 2.1 percentage points over a five-year period even though the company achieved revenue growth. This negative divergence signals deteriorating profitability on every dollar earned.

Investors scan for the opposite operational inflection point. They look for companies where revenue growth accelerates and operating margins expand simultaneously. This combination suggests that the business has covered fixed costs and now drops more profit to the bottom line with every new sale. Investors identify these trends early to adjust the growth assumptions in their valuation models and benefit from the market's lag in recognizing the efficiency gains.

The three recipes

Investors apply specific strategy recipes to capture different pockets of value across different market conditions. Recent data indicates value investing outperformed growth strategies during periods of higher inflation and rising interest rates in 2023 and 2024, but no single value recipe is best in every regime. The three recipes below are field-tested philosophies, each with its own filter parameters and its own ideal market conditions.

Recipe 1: Deep Value

This recipe seeks assets that trade below their liquidation value. It requires strict safety filters to avoid bankruptcy risk because cheap-on-paper companies are often cheap for structural reasons.

Filter parameters:

- Price-to-Book ratio under 1.0

- Debt-to-Equity ratio below 0.5

- Piotroski F-Score ≥ 6 (eliminates the worst balance-sheet deterioration cases)

- Positive free cash flow over the trailing twelve months

The P/B and D/E combination filters out companies that appear cheap simply because they carry excessive leverage. The F-Score adds a balance-sheet trend check on top of the static ratio. Without these safety checks, investors risk falling into value traps, where cheap stocks remain cheap due to structural issues rather than temporary mispricing.

When to use: Deep Value works best in depressed sectors and post-crisis markets where quality companies temporarily trade below intrinsic value. The recipe underperforms during established bull markets when truly cheap names are usually cheap for structural reasons.

Pitfalls: Skipping the D/E filter or the F-Score check turns this recipe into a value-trap generator. Many P/B < 1.0 candidates are structurally impaired businesses (declining industries, regulatory headwinds) rather than mispriced assets.

Recipe 2: Quality at a Reasonable Price (QARP)

This recipe targets excellent businesses that are temporarily out of favor. Instead of buying the cheapest names, it prioritizes earnings efficiency and accepts a modest valuation premium for that quality.

Filter parameters:

- Top decile of Return on Invested Capital (ROIC) within the chosen universe

- PEG ratio below 1.5

- Operating margin stable or expanding over the past 5 years

- Net debt to EBITDA below 2.5x

The ROIC filter ensures the business compounds capital efficiently. The PEG check guards against overpaying for the quality — many QARP candidates remain "reasonably priced" only when growth assumptions hold. The margin trend and debt covenants confirm the quality signal isn't being supported by one-off accounting choices.

When to use: QARP suits established bull markets where quality demands a premium and the strategy targets excellent businesses temporarily out of favor due to sector rotation or earnings noise. Less effective in depressed markets where Deep Value finds better risk-adjusted entries.

Pitfalls: Overpaying for "quality" when the ROIC is the result of inflated denominator games (aggressive buybacks reducing invested capital base). Verify the trend over multiple periods rather than relying on a single snapshot.

Recipe 3: Sector Rotation

This recipe identifies cyclical opportunities by comparing current valuations to a sector's own historical norm. Instead of finding cheap names across the whole market, it isolates one sector and looks for the cyclical bottom.

Filter parameters:

- Sector-specific filter (energy, materials, financials, etc.)

- Current sector P/E ratio significantly below its own 5-year average (>20% discount)

- Companies trading at the lower end of their own historical valuation band

- Balance sheet strong enough to survive the cyclical trough (interest coverage > 3x)

The sector-specific framing matters because cross-sector comparisons confuse cyclical lows with secular declines. A 20% P/E discount in semiconductors signals something very different from a 20% discount in coal.

When to use: Sector Rotation captures cyclical inflection points when a sector trades below its own historical average AFTER a broader risk-off move. Most useful 6-18 months after a sector-specific drawdown when fundamentals are bottoming.

Pitfalls: Catching falling knives in structurally declining sectors. The 5-year average isn't useful if the structural drivers have changed (e.g., coal in a decarbonizing economy). Pair the cyclical discount filter with a check on sector-level structural trends before deploying capital.

After the recipe: human validation

These strategies generate lists of potential candidates that require further verification. A scanner output acts as a lead list rather than a buy order. Even sophisticated market scanners rely on reported data that can contain errors or anomalies, or lack necessary context. Academic research highlights that data quality issues often require anomaly detection and consistency checks before investors can rely on the numbers for quantitative analysis. Consequently, investors subject the automated results to intense scrutiny and verification to ensure the investment thesis holds water.

The validation process involves three critical steps:

-

Verify Data Source: Investors compare the scanner's numbers against the company's official SEC filings (10-K and 10-Q). One-time charges, asset write-downs, or changes in accounting methods can distort the automated ratios used by stock scanners and make a stock appear artificially cheap or expensive.

-

Assess Qualitative Story: Investors investigate the qualitative factors that a scanner misses, such as regulatory threats, management changes, or pending litigation. This step determines whether the low valuation represents a market overreaction or a rational response to an existential threat.

-

Review Capital Allocation: Investors examine the cash flow statement and observe how management uses its profits. A company might pass the ROIC scan, but the theoretical value may never reach the shareholder if management hoards cash or makes reckless acquisitions.

Conclusion

To summarize, you now have three field-tested strategy recipes — Deep Value, Quality at a Reasonable Price, and Sector Rotation — with exact filter parameters, market conditions where each works best, and the specific pitfalls to avoid. None of these recipes is correct in every market regime. The discipline is to match the recipe to current conditions rather than treating one as a permanent rule.

After the recipe filters down to a candidate list, the human-validation step (above) and the broader fundamental analysis workflow close the loop. The recipe gives you the lead; the verification confirms whether the candidate survives deeper analysis.

For investors looking to put these recipes into practice, InvestViable offers the screening tools and valuation frameworks that support each step of this workflow. 19:T